What we do

We have a range of products

We are a leading international transport provider, diversified internationally and by business area.

![]()

Long distance coach

Inter-city, tourism and airport transfer services in the UK and Spain, providing a cheaper and often more convenient alternative to rail

![]()

Urban bus

Single and double decker bus services in busy cities and their suburbs, in the UK, Ireland, Spain, Portugal, Morocco and Bahrain.

![]()

Corporate shuttle

A range of services for transporting their employees to work; includes full hometo-work service and filling the “last mile” gap from mass transit hubs to the place of work.

![]()

Private hire

The provision of buses or coaches to individuals, employers, schools or other organisations for field trips, days out, holidays, etc.

![]()

Rail

We operate a number of lines in the southwest of Germany following a successful start of operations in 2015.

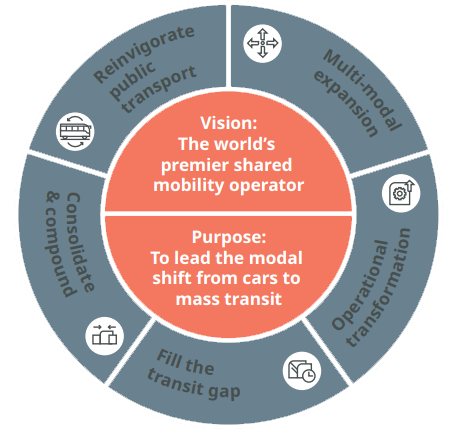

Customer propositions

Our products enable us to create solutions for our customers across each of our five Evolve customer propositions.

1. Reinvigorate public transport: grow use of public transport in cities suffering congestion by building partnerships with stakeholders who want sustainable solutions.

2. Multi-modal expansion: build more modal capability and city hubs from existing locations where we already have a physical footprint.

3. Operational transformation: application of our processes and know-how to drive efficiency, operational improvement and lower costs.

4. Fill the transit gap: encouraging modal shift away from private cars in areas that are not well served by public mass transit.

5. Consolidate & compound: consolidate fragmented markets and create ‘at scale’ operations to drive operating efficiencies and better customer solutions.

globally diversified contract models

We have a mix of contracted and non contracted revenues